Views: 1965

ROIC Formula 投资回报率公式

Return on Invested Capital is calculated by taking into account the cost of the investment and the returns generated. Returns are all the earnings acquired after taxes but before interest is paid. The value of an investment is calculated by subtracting all current long-term liabilities, those due within the year, from the company’s assets.投资资本回报率是通过考虑投资成本和产生的回报来计算的。回报是税后但在支付利息之前(息前税后)获得的所有收益。投资价值的计算方法是从公司资产中减去所有流动的长期负债,即当年内到期的长期负债。

The cost of investment can either be the total amount of assets a company requires to run its business or the amount of financing from creditors or shareholders. The return is then divided by the cost of investment.投资成本可以是公司经营业务所需的资产总额,也可以是债权人或股东的融资金额。然后将回报除以投资成本。

Note: NOPAT is equal to EBIT x (1 – tax rate) 注:NOPAT等于息税前利润x(1 – 税率)

A company’s return on invested capital can be calculated by using the following formula:公司的投资回报率可以通过使用以下公式计算:

The book value is considered more appropriate to use for this calculation than the market value. The return on capital invested calculated using market value for a rapidly growing company may result in a misleading number. The reason for this is that market value tends to incorporate future expectations.账面价值被认为比市场价值更适合用于此计算。对于一家快速增长的公司,使用市场价值计算的资本投资回报率可能会导致误导性数字。原因是市场价值倾向于包含未来预期。

Also, the market value gives the value of existing assets to reflect the business’ earning power. In a case where there are no growth assets, the market value may mean that the return on capital equals the cost of capital.此外,市场价值给出了现有资产的价值,以反映企业的盈利能力。在没有增长资产的情况下,市场价值可能意味着资本回报率等于资本成本。

To get the invested capital for firms with minority holdings in companies that are viewed as non-operating assets, the fixed assets are added to the working capital. Alternatively, for a company with long-term liabilities that are not regarded as a debt, add the fixed assets and the current assets and subtract current liabilities and cash to calculate the book value of invested capital.为了获得在被视为非经营性资产的公司中持有少数股权的公司的投资资本,固定资产被添加到营运资金中。或者,对于长期负债不被视为债务的公司,将固定资产和流动资产相加,减去流动负债和现金,以计算投资资本的账面价值。

The return on invested capital should reflect the total returns earned on the capital invested in all of the projects listed on the company’s books, with that amount compared to the company’s cost of capital.投资资本回报率应反映投资于公司账簿上列出的所有项目的资本的总回报,该金额与公司的资本成本进行比较。

ROIC的计算公式比较多,常见的有以下几种:

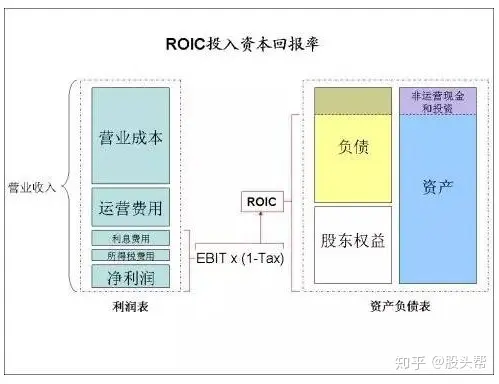

(1)ROIC=息税前收益(EBIT)*(1-税率)/(净资产+有息负债)

[息税前利润(EBIT) = 营业收入 – 营业成本 – 营业费用 + 营业外收入支出 (或是税前净利 + 利息费用)], 其中有息负债包括:短期借款、长期借款、应付债

(2) ROIC = EBIT × (1 – 税率) ÷投入资本

投入资本 = 流动资产 – 流动负债 + 不动产与厂房设备净额 + 无形资产及商誉 (Net Working Capital + Property Plant and Equipment (PP&E) + Goodwill and Intangibles)

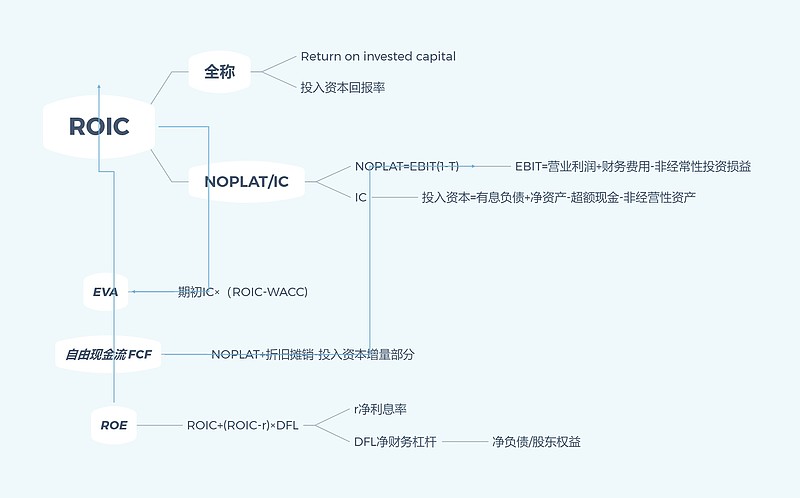

(3)ROIC=NOPAT/投入资本

其中NOPAT=(营业利润+利息支出)*(1-税率),称为税后净营业利润(NOPAT),投入资本=总资产-无息流动负债-商誉,

无息流动负债=应付票据+应付账款+预收款项+应付职工薪酬+应交税费+其他应付款+预提费用+流动负债中递延收益+其他流动负债

(4)ROIC=息前税后经营利润/投入资本=EBIT(1-T)/IC

=(营业利润+财务费用-非经常性损益)(1-所得税)/(有息负债+净资产-超额现金-非经营性资产)

(5)投入资本 为 Total Debt and Leases + Total Equity and Equity Equivalents + Non-Operating Cash and Investments.投入资本 为债务和租赁总额+权益和权益等价物总额+营业外现金和投资。

尽管有不同算法,但大致上的意思就是公司把短期可能需用到(例如:拿去还短期负债、应付帐款)的资产扣掉,剩下的就是长期能动用的资产,也就是一家公司保持营运所需投入的资本,投入资本介于总资产与总股东权益之间,概念上近似于股东权益加上长期负债并扣除多余现金,这两种都属于企业用于长期规划的。

ROIC是生产经营活动中所有投入资本赚取的收益率,而不论这些投入资本是被称为债务还是权益,它度量的是企业全部投资资本的收益率。所以,计算ROIC的关键是对公司业务能进行快速分解,快速阅读公司资产负债表及报表附注,分解出公司的“核心资产”和“非核心资产”。

ROIC也称投入资本回报率,用于衡量投出资金的使用效果。ROIC是生产经营活动中所有投入资本赚取的收益率,剔除了资本结构变动的影响,而不论这些投入资本是被称为债务还是权益。 ROIC是从资本的角度看问题,综合考虑股权与债权,衡量投资的效率,与ROIC对应的是平均资金成本(WACC),如果ROIC小于WACC,就说明投入资本的回报小于平均资本成本,公司是在浪费资本。

ROIC越大,代表公司投入的资本创造越多业主盈余。所以,ROIC也是投资人评估公司是否有效利用资本赚取超额报酬的其中一项指标。

为什么要计算ROIC?

1.用ROIC和公司资金机会成本做比较评估获利能力

ROIC通常会拿来跟公司的加权平均资本成本(WACC)做比较,去评估公司投入的资本是否有创造超额报酬。

原因是WACC代表公司向银行或是股东借来的钱,WACC算出来的金额可想成是利息费用或机会成本的概念,简单来说,如果ROIC大于WACC,就代表公司投入资本后所获得的报酬大于公司因借钱去投入所产生的成本(例如:跟银行借钱去开餐厅,每个月餐厅所赚的钱大于要还银行的利息费用),也就是公司有利用投入的资本创造超额报酬。

举例来说,假设一间公司跟银行借100元(先假设股东没出钱),利息是5%,WACC=5%,每年就要还银行5元,

那ROIC至少要超过5%,这样才可能会有超额报酬,不然每年赚5元马上又要还银行5元,等于完全没有赚钱。

所以,我们可以将ROIC与WACC之间的关系做一个比较:

| ROIC > WACC | 公司投入资本的报酬>投入的资本成本, 有创造超额报酬 |

| ROIC = WACC | 公司投入资本的报酬 = 投入的资本成本,没有创造超额报酬 |

| ROIC < WACC | 公司投入资本的报酬 < 投入的资本成本,不但没有创造超额报酬,还破坏公司本身的价值(破坏公司本身的价值这一点跟计算现值有关,比较复杂一些,先知道概念即可) |

2. 用ROIC来预估公司未来盈余成长率

评估EPS成长率有很多种方式,其中一个算法就会用到ROIC。

一间公司的有机成长,就是运用公司赚到的钱,扣除发放股利后,剩余部分再投资创造报酬,其中,再投资创造报酬的报酬率,就可以用ROIC来做评估。

公司预期EPS成长率 = 再投资比率(Reinvestment rate) × ROIC

其中,再投资比率就是有多少盈余是没发放股利的部分。

再投资比率(Reinvestment rate)=1 – 股利发放率(就是配息率)

ROIC可视为ROA与ROE的进化版

有些人会把ROIC解读成资产回报率(ROA)及净资产收益率(ROE)的优化版:

· 投入资本回报率率(ROIC) = EBIT × (1 – 税率)÷投入资本

· 资产回报率(ROA)= 税后净利 ÷ 平均总资产 × 100%

· 净资产收益率(ROE) = 税后净利 ÷ 股东权益 × 100%

以ROA来看,ROA是以总资产为分母去看公司能产生的报酬,这会有个问题是,如果是短期负债庞大的企业 (例如因为营运周转需求,产生庞大的应付帐款、短期负债等等),这会导致ROA在评估结果产生误差。

ROIC的分母则是将流动负债扣除,只保留长期营运的资本投入(股东权益+长期负债),不考虑短期负债(例如应收帐款、短期负债),且ROIC的分子排除掉业外收支的影响,

所以整体来说ROIC会比ROA更严谨一些。

以ROE来看,因为ROE的分母是股东权益,没算到负债,如果企业靠增加债务杠杆来扩大获利,这种举债行为并不会对股东权益造成影响,所以ROE就会变高,但ROIC的分母是投入资本,在计算时会考虑长期负债,就可以避免企业高度杠杆而冲高数字的结果。

另外,相比ROA及ROE的分子是税后净利,ROIC的分子是税后营业收入或税后营业利润(EBIT也就是还没扣除利息及税的费用),能避免企业因为借钱(跟银行借或是跟股东借)产生利息费用而影响到计算的结果,更能看出企业本身的营业获利能力。

息税前利润EBIT(Earnings Before Interest and Tax)

How to Interpret ROIC? 如何解释 ROIC?

Generally, the higher the return on invested capital (ROIC), the more likely the company is to achieve sustainable long-term value creation. 一般来说,投资资本回报率(ROIC)越高,公司就越有可能实现可持续的长期价值创造。

- 50% ROIC → A 50% ROIC means that a company provided with $1.00 in funding is able to reinvest those proceeds to turn the investment into $1.50. → 50%的ROIC意味着获得1.00美元资金的公司能够将这些收益再投资,将投资转化为1.50美元。

- 25% ROIC → In comparison, a 25% ROIC means that the company turned the $1.00 into $1.25 instead, so it should be straightforward to understand that a higher ROIC ratio is preferrable. 相比之下,25% 的 ROIC 意味着该公司将 1.00 美元变成了 1.25 美元,因此应该很容易理解更高的 ROIC 比率是可取的。

Companies with high returns on invested capital are more likely to continue employing capital thoughtfully to achieve returns in line with the past (or similar) – it is usually very rare to come across such opportunities at the right time and share price. 投资资本回报率高的公司更有可能继续深思熟虑地利用资本来实现与过去(或类似)一致的回报——在正确的时间和股价遇到这样的机会通常非常罕见。

Source:

Return on Capital Employed (ROCE): Ratio, Interpretation, and Example (investopedia.com)

What is Return on Invested Capital? (ROIC) | Formula + Calculator (wallstreetprep.com)

粤ICP备2022015479号-1 All Rights Reserved © 2017-2023

粤ICP备2022015479号-1 All Rights Reserved © 2017-2023